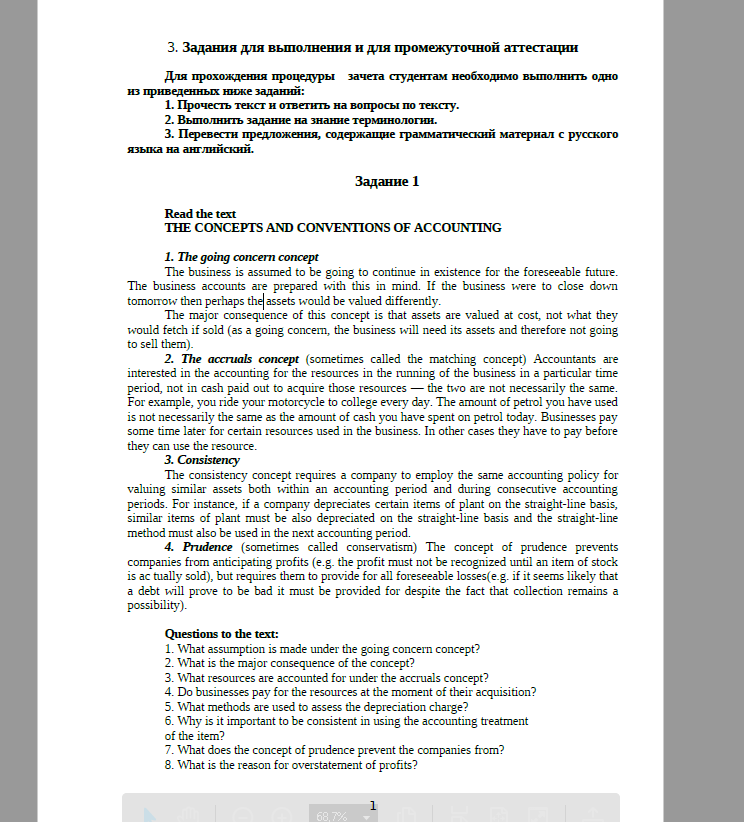

Описание

Read the text

THE CONCEPTS AND CONVENTIONS OF ACCOUNTING

1. The going concern concept

The business is assumed to be going to continue in existence for the foreseeable future.

The business accounts are prepared with this in mind. If the business were to close down tomorrow then perhaps the assets would be valued differently.

The major consequence of this concept is that assets are valued at cost, not what they would fetch if sold (as a going concern, the business will need its assets and therefore not going to sell them).

2. The accruals concept (sometimes called the matching concept) Accountants are interested in the accounting for the resources in the running of the business in a particular time period, not in cash paid out to acquire those resources — the two are not necessarily the same.

For example, you ride your motorcycle to college every day. The amount of petrol you have used is not necessarily the same as the amount of cash you have spent on petrol today. Businesses pay some time later for certain resources used in the business. In other cases they have to pay before they can use the resource.

3. Consistency

The consistency concept requires a company to employ the same accounting policy for valuing similar assets both within an accounting period and during consecutive accounting periods. For instance, if a company depreciates certain items of plant on the straight-line basis, similar items of plant must be also depreciated on the straight-line basis and the straight-line method must also be used in the next accounting period.

4. Prudence (sometimes called conservatism) The concept of prudence prevents companies from anticipating profits (e.g. the profit must not be recognized until an item of stock is ac tually sold), but requires them to provide for all foreseeable losses(e.g. if it seems likely that a debt will prove to be bad it must be provided for despite the fact that collection remains a possibility).

Questions to the text:

1. What assumption is made under the going concern concept?

2. What is the major consequence of the concept?

3. What resources are accounted for under the accruals concept?

4. Do businesses pay for the resources at the moment of their acquisition?

5. What methods are used to assess the depreciation charge?

6. Why is it important to be consistent in using the accounting treatment of the item?

7. What does the concept of prudence prevent the companies from?

8. What is the reason for overstatement of profits?

Give English equivalents for:

комитет бухгалтерских стандартов

бухгалтерский отчет

основные принципы бухгалтерского учета

метод начисления амортизации основных активов

метод оценки запасов и незавершенного производcтва

учет и амортизация нематериальных активов

бухгалтерская политика

принцип непрерывности деятельности

оценить активы по себестоимости

принцип начисления

учет ресурсов

платить наличными

принцип постоянства правил бухгалтерского учета

бухгалтерская политика

принцип осмотрительности

возможные потери

Translate into English Using Passive Voice and Constructions with Non-Finite Forms of the Verb

1. Оперативный учет используется для оперативного планирования и текущего управления. Его ведут там, где производится продукция предприятия и выполняются хозяйственные функции, то есть в цехах и службах. Данные оперативного учета используются внутри предприятия.

2. На Западе используются также принципы оценки имущества и обязательств, двойной записи хозяйственных операций, осторожности, существенности, доброкачественности информации и др.

Методы оценки имущества и обязательств регламентированы не жестко, применяется метод «исторической оценки», т. е. оценки имущества и обязательств на дату совершения операции. Есть ряд способов перехода от «исторической оценки» к реальной.